Growth is not a victim of the UPA, it is the other way round

It is said that UPA faces voter wrath because it destroyed growth. If you look at data for the last 10 years, and compare with figures from the NDA days, you may be in for a surprise, write Maitreesh Ghatak and Parikshit Ghosh.

If the opinion polls are to be believed, the UPA is facing a rout in the coming Lok Sabha elections. One explanation, popular in the media, goes something like this: The UPA faces voter wrath because it destroyed growth. The economy has paid a price for bad governance and expensive welfare schemes. If you look at data for the last two years, this view will find some support. The growth rate has halved, the fiscal deficit has doubled, the rupee suffered a steep decline last summer, and the overall economic mood seems bleak.

If you look at data for the last 10 years, and compare with corresponding figures from the NDA days (1998–2004), you may be in for a surprise. Under the UPA, growth accelerated, the stock market boomed, Indians saved and invested more, money poured into building infrastructure and foreign direct investment went through the roof. The 2008 financial crisis reached these shores like any other, but the economy recovered quickly, and continued on its high growth path for another two years.

Make no mistake, the Congress has dropped the ball politically — its leadership crisis is apparent to anyone who is paying attention. On the policy front too, it has made serious mistakes. But this article is not about politics or policy, it is about results. Whether aided by fortune or skill, the UPA presided over one of the strongest decades for the Indian economy. This fact is getting drowned in the drumbeat of the elections. The truth is often the first casualty of politics.

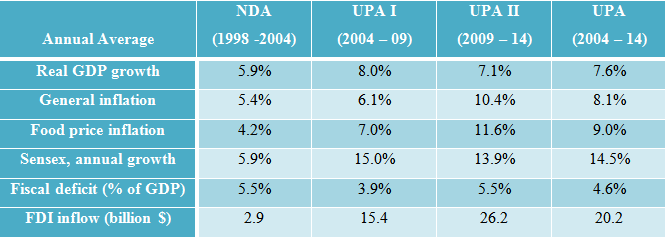

The table above presents some key economic indicators for the NDA and the UPA years. All figures are average annual rates. India’s GDP grew at nearly 6% per year on average under the NDA, accelerated to 8% under UPA 1 and has slipped back to 7% under UPA 2. On the whole, the economy grew 1.5 percentage points faster under the UPA than under the NDA.

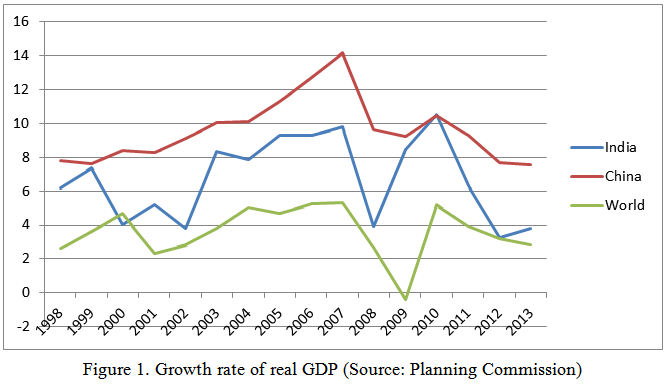

If we compare India’s growth rates over the last two decades alongside China’s and the world’s, we will find that we have always been somewhere in between with very similar fluctuations (see figure 1). In an age of globalisation, attributing the ups and downs of national economies entirely to the wisdom or folly of those in power is a mistake.

Nevertheless, India grew 2.5 percentage points faster than the world as a whole during the NDA, which has increased to about 3.5 percentage points under the UPA. The UPA leadership can claim some credit for increasing the growth lead.

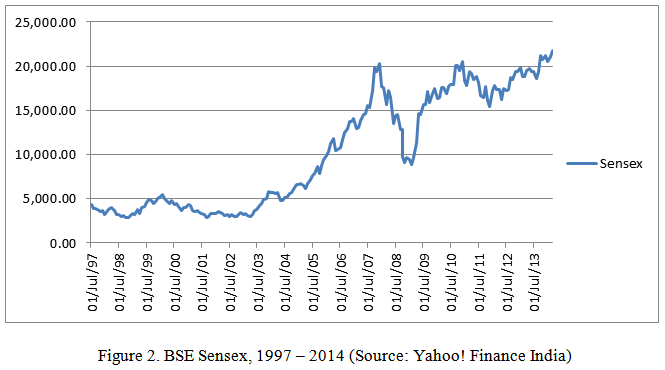

The stock market also boomed after the UPA came to power (see figure 3). The index grew at nearly 6% during the NDA years, but jumped to 14 -15% under the UPA. Even if one takes into account the higher inflation of those years, stocks gained much more in real terms under the UPA than under the NDA. If history is their guide, Dalal Street and India Inc. should be throwing their weight behind the incumbent in the coming general elections.

The story of the deficit and the rupee that one hears these days, like the growth story, draws on short-term memory. The increase in subsidies under the UPA has been offset by cuts in defence spending. Adjusted for the size of the economy, the fiscal deficit today is where it was during the NDA years (between 5 and 6% of GDP). People expect better only because the UPA had steadily reduced it to 2.5% over its first term before the financial crisis of 2008 (and not the launch of MGNREGs in 2006) caused a sharp spike. The rupee has slid in nominal terms but not so much in real terms, but inflation has been admittedly higher under the UPA (see table).

To understand what really went wrong (and right) under the UPA, we must focus on two significant developments during its tenure, both of which should shred its reputation as being lukewarm towards markets and growth. There was a surge in FDI, and investment in infrastructure picked up with the infusion of private capital and public-private-partnership projects.

Annual FDI inflows into India went from an average of $2.9 billion during the NDA’s rule to $26.2 billion under UPA 2, nearly a 10-fold increase. According to Planning Commission figures, spending on infrastructure went up from around 5% of GDP annually under the NDA to 7-8% underthe UPA, even though public spending remained roughly the same. A traditionally state-dominated sector was opened up to private enterprise and even foreign funds to boost growth.

If you remember some of the mega scams that hit the UPA (2G, Coalgate), they involve the entry of private capital into sectors like power, minerals, telecom and construction. In Transparency International’s corruption perception index, India’s average rank slipped from 75th to 85th as the UPA took over from the NDA.

The government was unable (or unwilling) to give up its culture of discretionary decision making and opt for a culture of transparency — open bidding, rational pricing and clear rules of allocation. Even as infrastructure fed growth and laid the foundations of future prosperity, it produced massive amounts of ill-begotten wealth. Land acquisition became both an obstacle for industries and a source of farmers’ agitations.

The idea that the UPA’s populist pro-poor welfare schemes busted the budget and stopped the growth engine is a myth. Growth is not a victim of the UPA, it is the other way round. The ruling party was unable to handle the stress and inequities it generated. It didn’t suppress growth, it let it run amok.

Autocratic, Superman-style swift governance that is cosy with big business is hardly the answer. Nor an anti-corruption crusade that shoots first and asks questions later. The principal opposition parties have harvested the disaffection very well but offer development dreams and demagoguery more than solutions. As India goes to the polls, voters have reasons to throw out the Congress but hardly a better alternative.

Maitreesh Ghatak is professor of economics, London School of Economics, and Parikshit Ghosh is associate professor of economics, Delhi School of Economics

The views expressed by the authors are personal