E-Paper

E-Paper

Key numbers, ideas in the Economic Survey

The Survey’s projections, in line with the IMF’s latest growth projections, mean that India will go back to being the world’s fastest growing major economy in 2021-22 and 2022-23.

The Economic Survey 2020-21 released on Friday said that a vaccine drive and rebound in consumer demand will help India emerge from the carnage inflicted by the coronavirus pandemic and the lockdown imposed to slow its spread, with a V-shaped recovery in the economy. It added that India’s GDP growth is expected to jump to 11% in 2021-22. A snapshot of the key numbers and ideas presented in the survey

_1611960928516_1611960942473.JPG "Office workers work amid a busy day in a startup company in Mumbai. (HT Archive)")

Also Read: Policy response has ensured V-shaped recovery underway

1. Survey claims V-shaped recovery, while critics maintain it is K-shaped

In keeping with its prognosis of an ongoing V-shaped recovery in the economy, the Economic Survey has projected a GDP growth rate of 11% and 6.8% in 2021-22 and 2022-23. The Survey has also projected a nominal GDP growth of 15.4% in 2021-22. Nominal GDP numbers matters because they form the base of tax projections in the budget. The Survey’s projections, in line with the IMF’s latest growth projections, mean that India will go back to being the world’s fastest growing major economy in 2021-22 and 2022-23. To be sure, many independent economists do not share the official view regarding a V-shaped recovery and maintain that what is happening currently is a K-shaped recovery, where one part of the economy is growing faster than others.

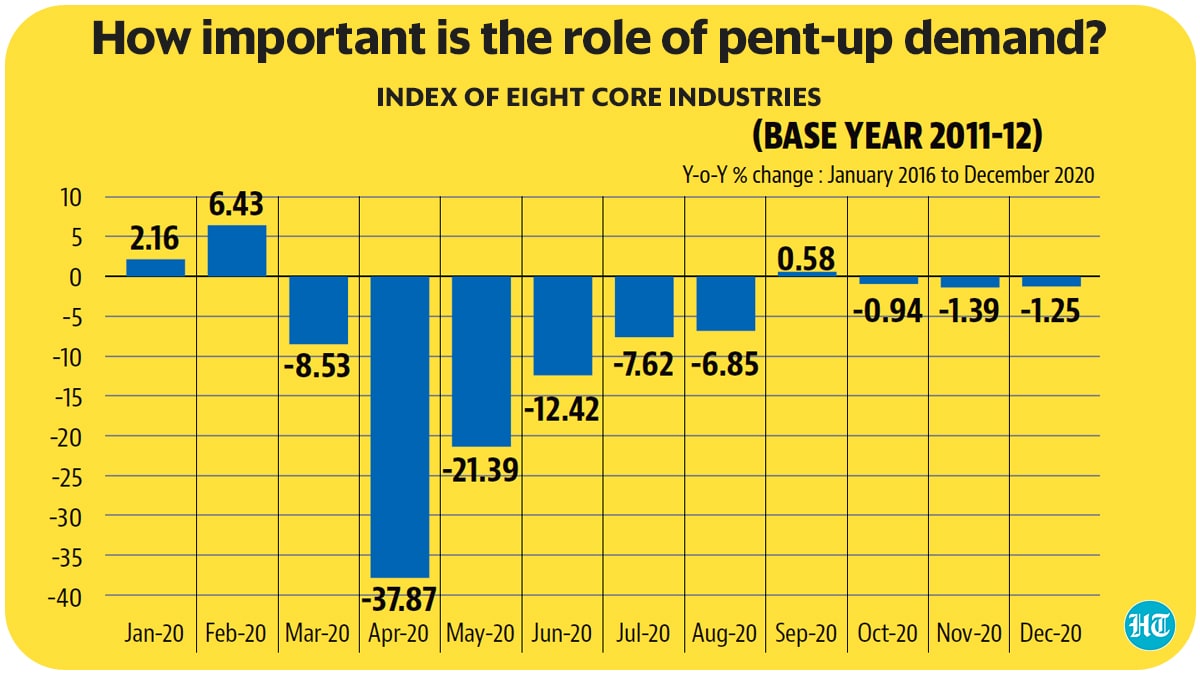

2. How important is the role of pent-up demand?

While it is common practice to extrapolate high frequency indicators to project growth rates, and this has only become more widespread during the pandemic, many economists have been pointing out that pent-up demand may be wrongly interpreted as a sustainable revival.

Clarity will emerge when the December quarter GDP numbers are released in the end of February.

However, the index of eight core sector industries contracted for the third consecutive month in December 2020, suggesting that core economic activity might not be out of the woods yet.

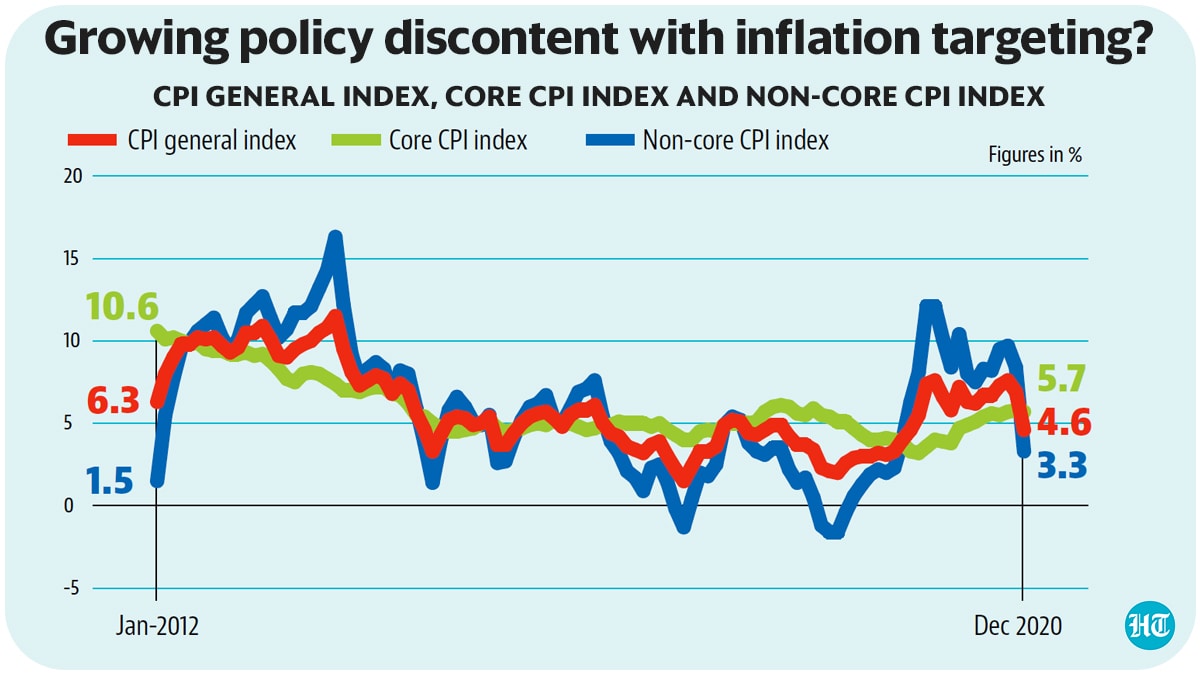

3. Growing policy discontent with inflation targeting?

Monetary policy, not fiscal policy, was the pro-active policy instrument in India’s initial response to the pandemic’s economic disruption. However, with retail inflation rising sharply after the lockdown – it remained above the upper limit of RBI’s tolerance band of four plus minus two percent from April to Nov 2020 – this has stopped being an option. The inflation target is coming up for revision this year and HT reported that the government might upwardly revise the target range of inflation. The survey has made an additional argument against using the current headline inflation numbers for policy making, by pointing out that it is heavily driven by food inflation, which is largely a supply-side issue. The survey also argues that more importance should be given to core inflation – the non-food non-fuel component of retail inflation – in the future.

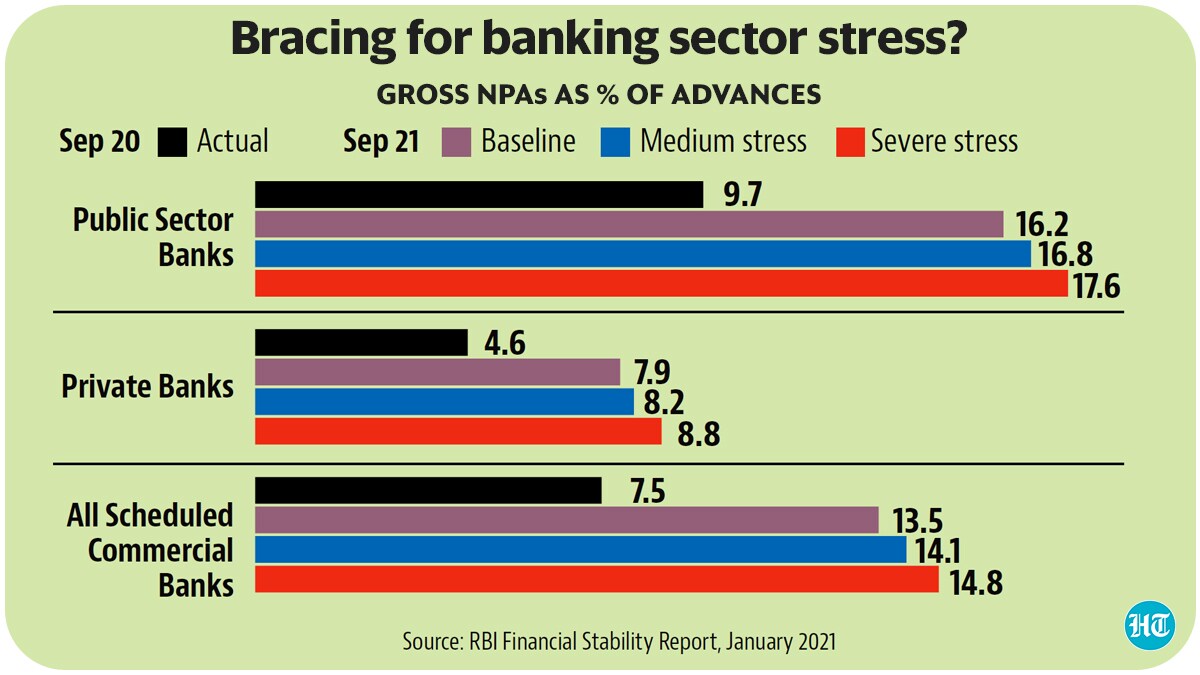

4. Bracing for banking sector stress?

One of the most damaging and systemic impacts of the previous economic disruption to the Indian economy (the 2008 global financial crisis) was the huge pile-up of bad debt in India’s banking sector. Over time, this has spread to non-banking financial companies and precipitated what is now termed as a four balance sheet problem in the economy. The pandemic’s disruption to business incomes is expected to lead to a large increase in bad loans, the real extent of which is not apparent at the moment because of regulatory forbearance (or banks being allowed to not make provisions for impaired assets). The Survey has made a strong case for seeing such forbearance as an emergency measure, and argued that an Asset Quality Review should be conducted as soon as this ends so that banks do not underestimate the amount of non-performing assets on their books.

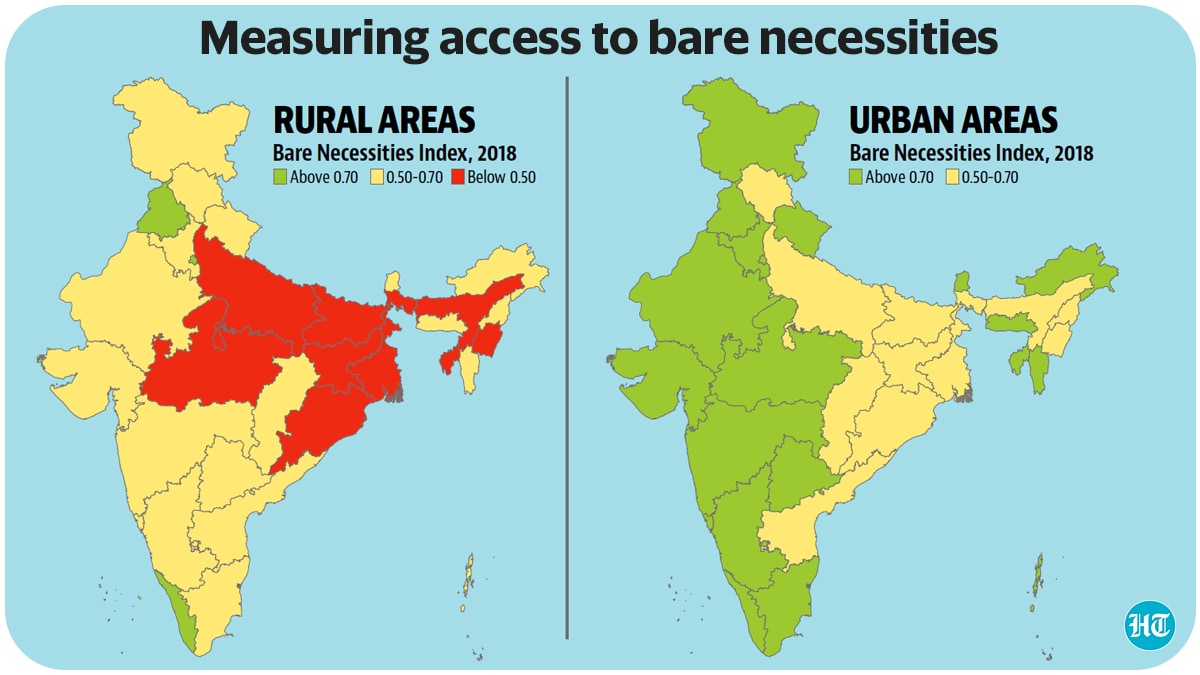

5. Measuring access to bare necessities

The Economic Survey 2020-21 has constructed a Bare Necessities Index, a composite measure of access to bare necessities for households in rural and urban India, for the years 2012 and 2018. The index is based on 26 comparable indicators on five dimensions – water, sanitation, housing, micro-environment, and other facilities. Between 2012 and 2018, access to the bare necessities has improved across states and the disparity between the states has reduced. A look at the 2018 figures shows that people in southern and western states are generally better placed in terms of having access to the bare necessities.