E-Paper

E-Paper

Tracking India’s past crisis budgets

Since Independence, India has faced different economic and social crises that have threatened to derail its growth. HT looks at the trajectory the budgets took then as we gear up for this year’s Union Budget that will come in the backdrop of the largest GDP contraction post-1947

The 2021-22 Union Budget will come in the backdrop of the largest GDP contraction India has suffered post-Independence. The National Statistical Office has projected a 7.7% contraction in GDP in 2020-21. There are only four previous instances when GDP growth has suffered a contraction in India: 1957-58 (1.2%), 1965-66 (3.7%), 1972-73 (0.3%) and 1979-80 (5.2%). Except in 1979-80, GDP contraction was driven entirely by a fall in agricultural production in each of these periods. Even in 1979-80, non-agricultural production fell by just 0.8% whereas agricultural production suffered a contraction of 12.8%.

")

To be sure, a GDP contraction need not be the only factor which makes a finance minister’s budget calculations very difficult. The Indian economy was on the brink of a balance of payment default when Manmohan Singh presented his first budget as a finance minister in 1991. The economy was at tenterhooks in the late 1990s when major economies of south-east Asia were engulfed in what is now referred to as the Asian crisis. The year after the 2008 global financial crisis was also a challenging time for economic policy.

How did economic policy cope with these challenges? What was the trajectory the budget took? Budgetary statistics for the period before 1990s are not given as systematically as they are presented now. Figures such as fiscal deficit, government spending etc. are not available in the Reserve Bank of India database for the period before 1970-71. Even the budget archives available on the ministry of finance website do not have the documents for 1965-66, 1968-69, 1970-71 and 1976-77. This makes it difficult to analyse long-term trends in budgetary numbers. With these caveats in mind, it is useful to look at the available statistics.

The contraction years

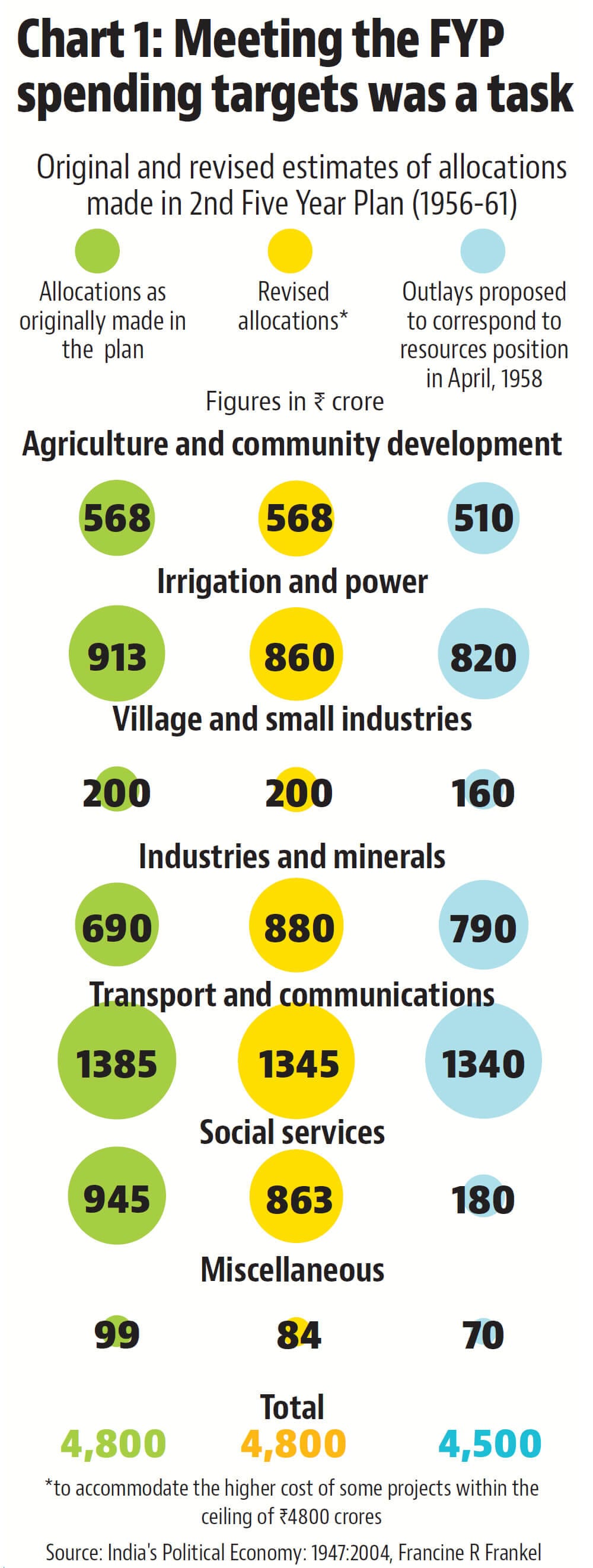

1957-58: The fall in GDP was driven by a collapse in agricultural production, not uncommon in the pre-green revolution phase. The contraction came despite the fact that central government spending grew at 17% and 23% in 1956-57 and 1957-58. India’s first post contraction budget ended up increasing the size of government spending by just 5.1%. GDP growth jumped to 7.6% in 1958-59.

To be sure, Five Year Plans (FYP) were more important than union budgets during this period, as spending goals were for five years, and fixed in advance. Thanks to various constraints, meeting the spending targets fixed in FYPs was a difficult task. The second FYP (1956-61) saw a mid-term cut ofRs 300 crore out of theRs 4,800 crore target which was set initially.

1965-66: While the GDP contraction was primarily in agriculture, this was also the year of an India-Pakistan war. This makes it difficult to do any meaningful comparison of government spending the year after, as defence spending must have taken a huge toll. Among the biggest fallouts of the economic shock of 1965-66 was a huge jump in inflation. Consumer Price Index for Industrial Workers (CPI-IW) grew at more than 12% in both 1966-67 and 1967-68. GDP growth was a mere 1% in 1966-67, implying that the economy did not come back to even 1964-65 levels in 1966-67.

The mid-1960s was a period of economic policy churn in India. The country had a new Prime Minister in Lal Bahadur Shastri after Jawaharlal Nehru’s death in 1964. The biggest effect of this on economic policy was the beginning of a rethink on replacing India’s public sector led five year plan (FYP) based economic model with a policy which allowed more space to domestic and foreign private capital.

Francine Frankel’s seminal book, India’s Political Economy 1947-2004 captures this well. Shastri taking over as the Prime Minister saw “a whole series of negotiations to attract foreign capital”, with the petroleum ministry entering into negotiations with the US Bechtels International for a joint project to set-up five large fertiliser factories in India. Shastri was also “increasingly influenced by his official advisers to accept the business community’s arguments in favour of a period of “consolidation” in the public sector”, Frankel writes. There was also increasing pressure from the World Bank to devalue the rupee, a decision which was left to Indira Gandhi after Shastri’s untimely death in January 1966 in Tashkent. 1966 also saw the suspension of FYPs, or Plan Holidays, for three years.

1972-73: This was a year when rains failed. Data from the Centre for Monitoring Indian Economy (CMIE) shows that there was a 20.4% shortfall in monsoon rainfall compared to the long period average. While the fiscal deficit increased marginally in the 1974-75 Budget, government spending actually increased by just 8.6% compared to 46% in the 1973-74 Budget. GDP growth increased to 4.6% in 1973-74.

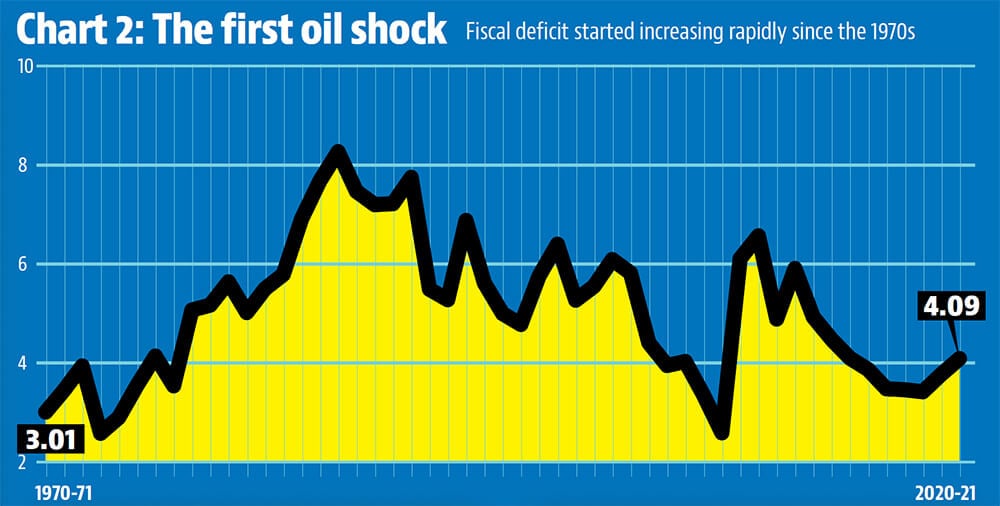

1973 was also the year of the first oil shock, when oil prices increased sharply. This had a huge impact on inflation. CPI-IW increased by 20.6% and 27.8% in 1973-74 and 1974-75. This was also the beginning of a rapid increase in India’s fiscal deficit. Fiscal deficit as a percentage of GDP was 3% in 1970-71. This number kept on increasing continuously to reach 7.8% in 1988-89.

1979-80: This was the year of the second oil shock with oil prices more than doubling in a year in the wake of the Iranian revolution. This was the first time when non-agricultural GDP also contracted in post-Independence India. CPI-IW jumped from 2.2% in 1978-79 to 8.8% in 1979-80 and 11.2% in 1980-81. Fiscal deficit maintained its upward trajectory. Government spending increased by 24% in the 1980-81 Budget, ten percentage points more than the 14.3% increase in 1979-80. GDP growth increased to 7.2% in 1980-81.

Non-contraction crisis years

1991-92: 1991 was a crisis year on many fronts. The 1990 Gulf War and worsening external balance in the past few years brought India to the brink of a default on the balance of payment front. This forced the government to mortgage India’s official gold reserves. GDP growth plummeted to 1.4% in 1991-92 and CPI-IW was in double digits in both 1990-91 and 1991-92. The 1991-92 Budget made a host of policy announcements to liberalise the Indian economy. While fiscal deficit as a share of GDP increased between 1990-91 and 1991-92 and growth in government spending came down sharply — it was 5.8% compared to 15.9%, 17.4% and 13.3% in the preceding three years — the reforms push gave a massive boost to GDP growth until 1997-98, when the Asian crisis generated a huge economic disruption. To be sure, both fiscal deficit and government spending growth remained elevated in the second half of the 1990s.

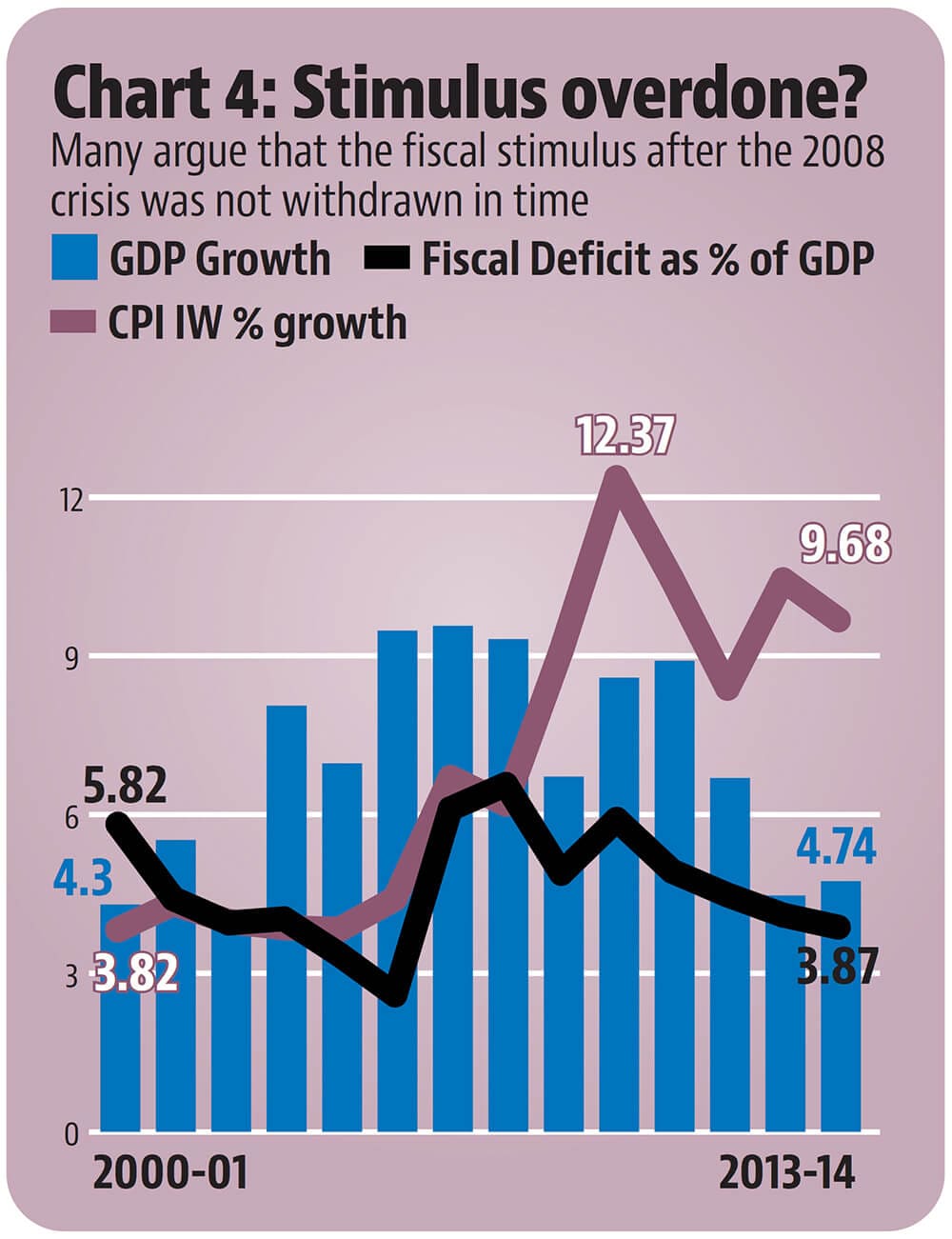

2009-10: The Global Financial Crisis (GFC) was the biggest economic disruption to the world economy since the Great Depression of the 1930s. Global GDP suffered a contraction of 1.6% in 2009. The Indian economy, which had been having a dream run before the GFC — it had grown at more than 9% between 2005-06 to 2007-08 according to the 2004-05 GDP series — managed to escape the worst effects of the global downturn, with GDP growth of 6.7% in 2008-09. This increased to 8.6% and 8.9% in 2009-10 and 2010-11. A fiscal boost played a big role in ensuring that India’s growth did not come down due to the GFC. Fiscal deficit, which had been falling continuously since 2000-01 and had come down to just 2.6% of GDP in 2005-06, increased to 6.6% in 2007-08 and stayed at 4.5% or more until 2011-12. The central government’s spending increased by more than 20% on an annual basis in 2007-08 and 2008-09. While the role of a fiscal stimulus in protecting growth is widely acknowledged during this period, many believe that the failure to withdraw this in time led to an overheating of the economy and culminated in a low growth-high deficit-high inflation-high current account deficit scenario in the first half of the last decade.

2009-10: The Global Financial Crisis (GFC) was the biggest economic disruption to the world economy since the Great Depression of the 1930s. Global GDP suffered a contraction of 1.6% in 2009. The Indian economy, which had been having a dream run before the GFC — it had grown at more than 9% between 2005-06 to 2007-08 according to the 2004-05 GDP series — managed to escape the worst effects of the global downturn, with GDP growth of 6.7% in 2008-09. This increased to 8.6% and 8.9% in 2009-10 and 2010-11. A fiscal boost played a big role in ensuring that India’s growth did not come down due to the GFC. Fiscal deficit, which had been falling continuously since 2000-01 and had come down to just 2.6% of GDP in 2005-06, increased to 6.6% in 2007-08 and stayed at 4.5% or more until 2011-12. The central government’s spending increased by more than 20% on an annual basis in 2007-08 and 2008-09. While the role of a fiscal stimulus in protecting growth is widely acknowledged during this period, many believe that the failure to withdraw this in time led to an overheating of the economy and culminated in a low growth-high deficit-high inflation-high current account deficit scenario in the first half of the last decade.

(Vineet Sachdev contributed to the data work for this story)