E-Paper

E-Paper

Rural demand engine choking once again?

The biggest reason for this seems to be the usual culprit, a worsening of the terms of trade against farmers. However, the weakness in labour markets in the cities is also contributing to the crisis. Here are four points that explain these trends.

When India announced an almost complete lockdown beginning on March 25, 2020 to prevent the spread of Covid-19 infections, economic activity suffered a sharp disruption. So much so that even the nation’s air and rivers became the cleanest they had been in years. The only sector that was an exception to this disruption was agriculture. With expected growth of 3.4% in 2020-21, it has emerged as a critical buffer for an economy that is set to suffer its biggest contraction ever in the financial year ending March. Agriculture’s performance has been critical for both maintaining supplies as well as sustaining rural demand. Recently released high-frequency indicators suggest that the rural demand story might be heading into rough weather once again. The biggest reason for this seems to be the usual culprit, a worsening of the terms of trade against farmers. However, the weakness in labour markets in the cities is also contributing to the crisis. Here are four points that explain these trends.

")

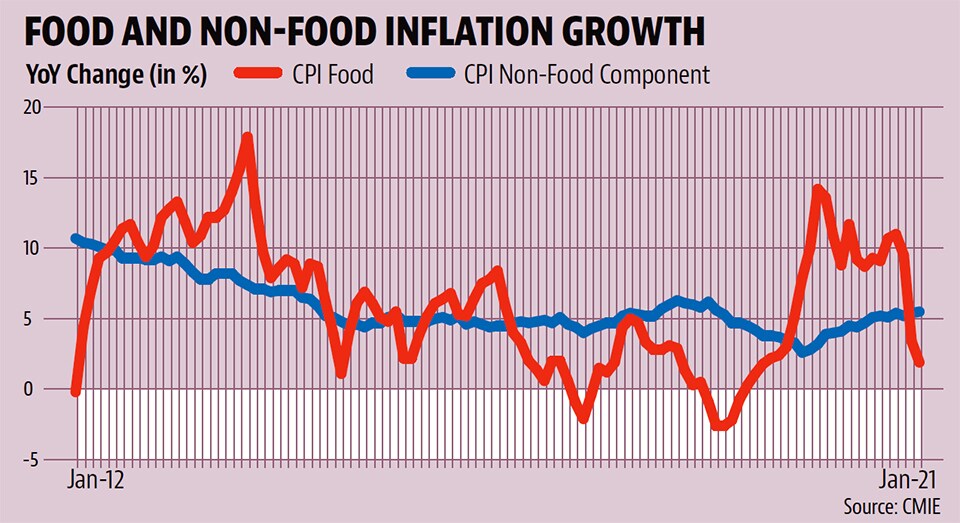

1. Food inflation has collapsed, but non-food prices continue to rise

According to the Consumer Price Index (CPI) data for January, which was released on February 12, food inflation has collapsed in the past two months. It grew 9.5% in November 2020, 3.4% in December 2020 and fell to 1.9% in January 2021. Non-food inflation, on the other hand, continues to increase, the respective numbers being 5.2%, 5.4% and 5.5%. The developing situation is the stark opposite of what existed in the past year or so when food inflation had been higher than non-food inflation. This entails a worsening of the terms of trade, or the ratio of prices of products they sell and buy, for the farmers.

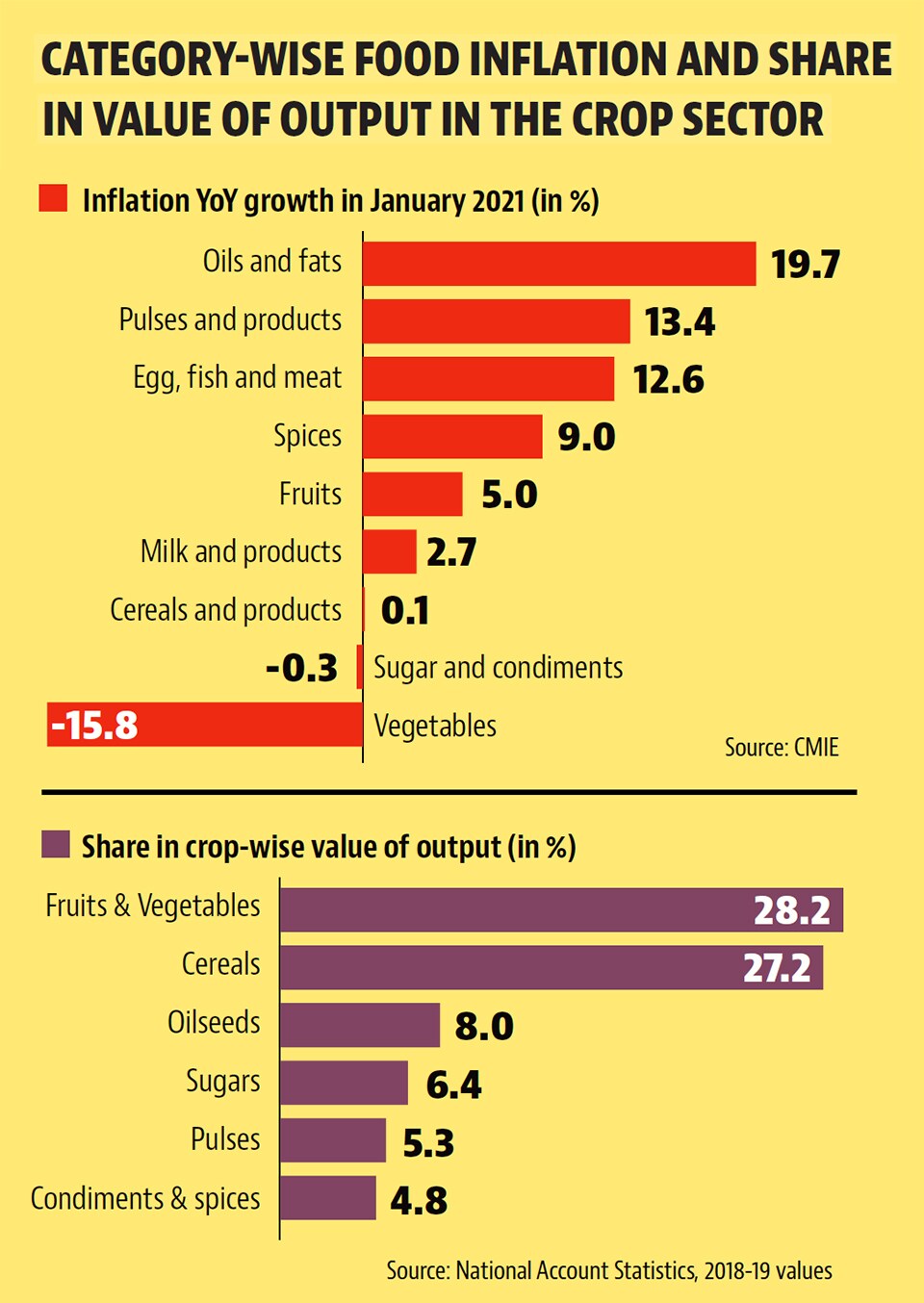

2. Fall in food inflation is being driven by items which matter in the agri-production basket

The sharp moderation in food prices, to be sure, is not a secular trend. While prices of vegetables have fallen sharply, and cereal prices remain flat, prices of other food items such as pulses, edible oils and meat products continue to rise in double digits. This means that the economic pain of worsening terms of trade vis-a-vis the food sector is confined to those who produce cereals and vegetables. An analysis of crop-wise share in the value of output in agriculture shows that cereals and vegetables are the most important component: they account for more than half of India’s agricultural production basket. This means that the numbers of farmers who would gain from a rise in prices of pulses and edible oil would be much smaller than those who are suffering because of the weakness in vegetable and cereal prices.

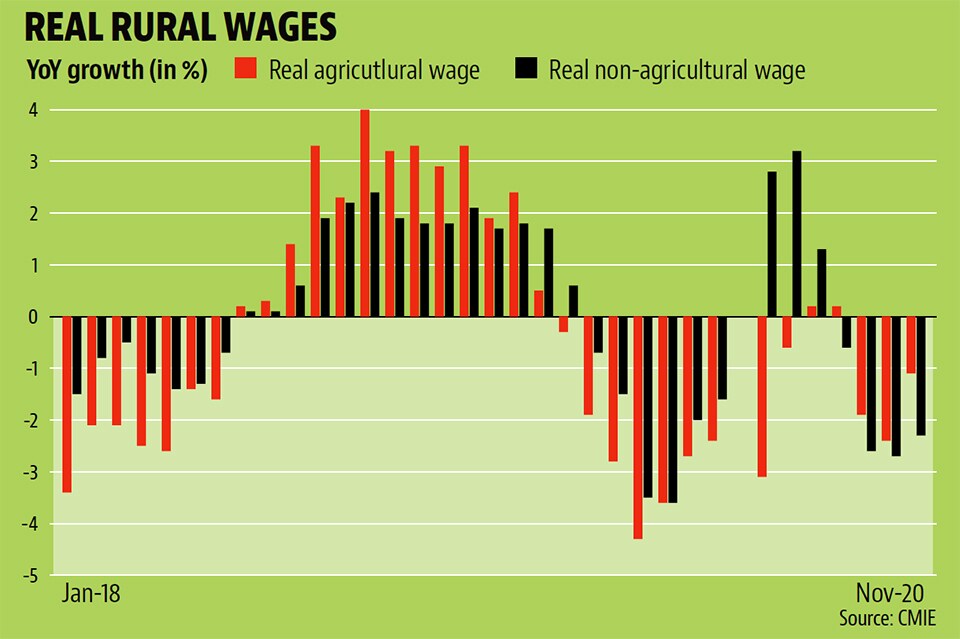

3. Real rural wages have been contracting for four months now

Monthly data on rural wages is the only government statistic to track labour markets on a high-frequency level. Given the practice of large-scale rural migration of unskilled workers, rural wages are considered to be a good proxy of conditions in urban labour markets as well. Real rural wages have been contracting continuously between August 2020 and November 2020 - the latest period for which data is available. When read with the fact that the October and November contraction has come on the back of an already low base, real rural wages contracted continuously between October 2019 and March 2020, the situation seems to be even more alarming. That non-agricultural wages have been falling at a faster pace than agricultural wages suggests that continuing weakness in urban markets – it is non-agricultural work which these labourers go and perform in cities – might be generating headwinds for wages in rural areas.

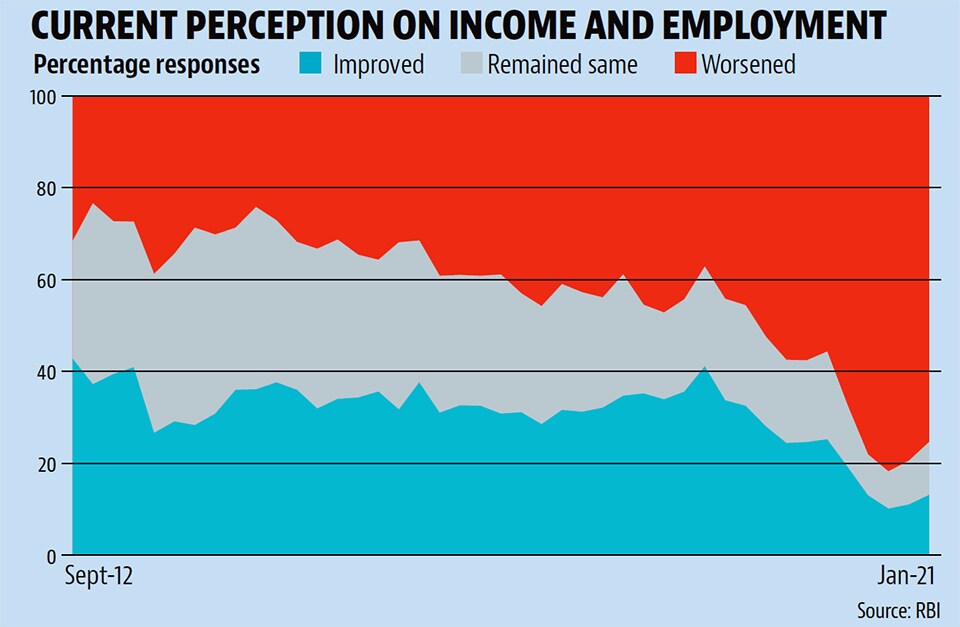

4. RBI consumer confidence survey data corroborates the urban labour market weakness story

While India does not have an official source of high-frequency data on employment, the Reserve Bank of India’s Consumer Confidence Surveys (CCS) offer an insight into prevailing sentiment vis-a-vis employment and incomes in the cities. The CCS is conducted every two months in the 13 biggest cities of India, the latest round having been done in January 2021. Among other things, the CCS seeks responses on perception around incomes and employment compared to a year ago. On both these counts, the share of respondents who reported a deterioration far exceeded those who reported an improvement, dragging the net perception into negative territory. The fact that things have not improved despite removal of lockdown restrictions and economic activity related private indices such a Purchasing Managers’ Indices and the Nomura India Business Resumption Index doing very well suggests that employment and wages continue to be weak even though production might be improving.

To be sure, experts have underlined the upside bias many high-frequency indicators including quarterly gross domestic product ( GDP) numbers could have. “Quarterly GDP data is less representative of informal sector, it could underestimate the extent of economic disruption and permanent scarring”, said a note by Samiran Chakraborty, chief economist India of Citi Research, while upgrading the growth forecast for 2020-21 GDP. Nomura economists Sonal Varma and Aurodeep Nandi noted that “labour and weak private capex conditions remain drags over (growth in) the medium term”.

“A collapse in vegetable prices and cereal incomes being flat at a time when non-food prices are rising will put a squeeze on farm incomes and hence rural demand. The fact that increased duties in petrol-diesel are major contributors to non-food prices suggests that this worsening of terms of trade for agriculture is partly policy inducedm” said Himanshu, an associate professor of economics at the Jawaharlal Nehru University. “We will do well to not become complacent about rural demand when the rest of the economy is still on thin ice,” he added.