E-Paper

E-Paper

Will 2021-22 fulfil economic goals?

The economy recovered sharply in the third and fourth quarters, expanding by 0.5% and 1.6% respectively, resulting in the overall contraction for the year being lower than the expected 8%. Things appeared to be on an upswing

RBI expects the economy to expand 9.5% in 2021-22. Where do things stand at the end of the first quarter?

")

The pandemic’s economic disruption forced a contraction of 7.3% in the Indian economy in 2020-21. The contraction was not homogenous throughout the year. It was the first quarter, the period from April to June 2020, which fared the worst with a contraction of 24.4%. This was basically the result of the 68-day-long hard lockdown which was imposed from March 25, 2020 onwards.

The economy recovered sharply in the third and fourth quarters, expanding by 0.5% and 1.6% respectively, resulting in the overall contraction for the year being lower than the expected 8%. Things appeared to be on an upswing. Then came the debilitating second wave of the pandemic, and lockdowns across the country. Where do things stand at the end of the March-June quarter, the first of 2021-22?

1. RBI does not see the economy regaining pre-pandemic levels in April-June quarter

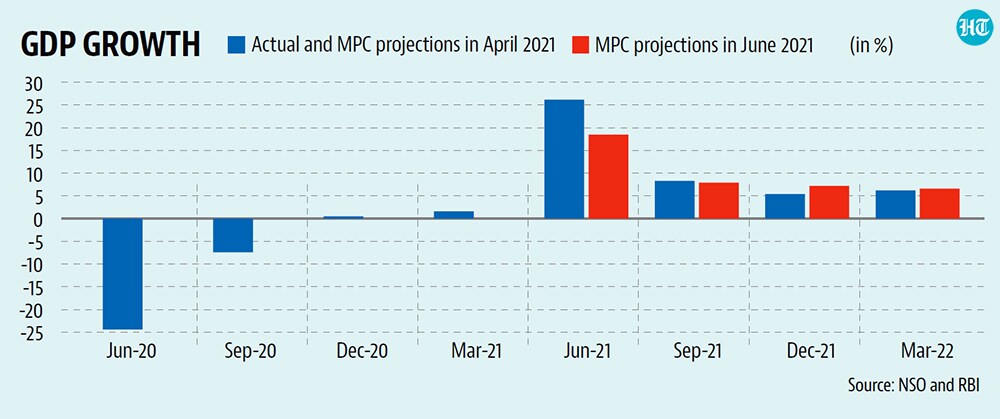

Because economic indicators collapsed due to the nationwide lockdown last year, the usual year-on-year comparisons are not very useful to measure the extent of recovery (or lack of it). The crucial question is whether the economy has regained pre-pandemic levels or not. The April meeting of the Monetary Policy Committee (MPC) of RBI saw this happening and projected a growth rate of 26.2% (last year’s contraction was 24.4%) in the first quarter.

This assessment was discarded in the next MPC meeting held in the first week of June and the MPC brought down its growth projection for the quarter ending June 30 to 18.5%. This means that GDP in the quarter ended June will be lower than what it was in June 2019. To be sure, many economists believe that the impact of the second wave has been softer than that of the first wave, most likely a result of the fact that there was no national lockdown. High frequency indicators can throw more light on this.

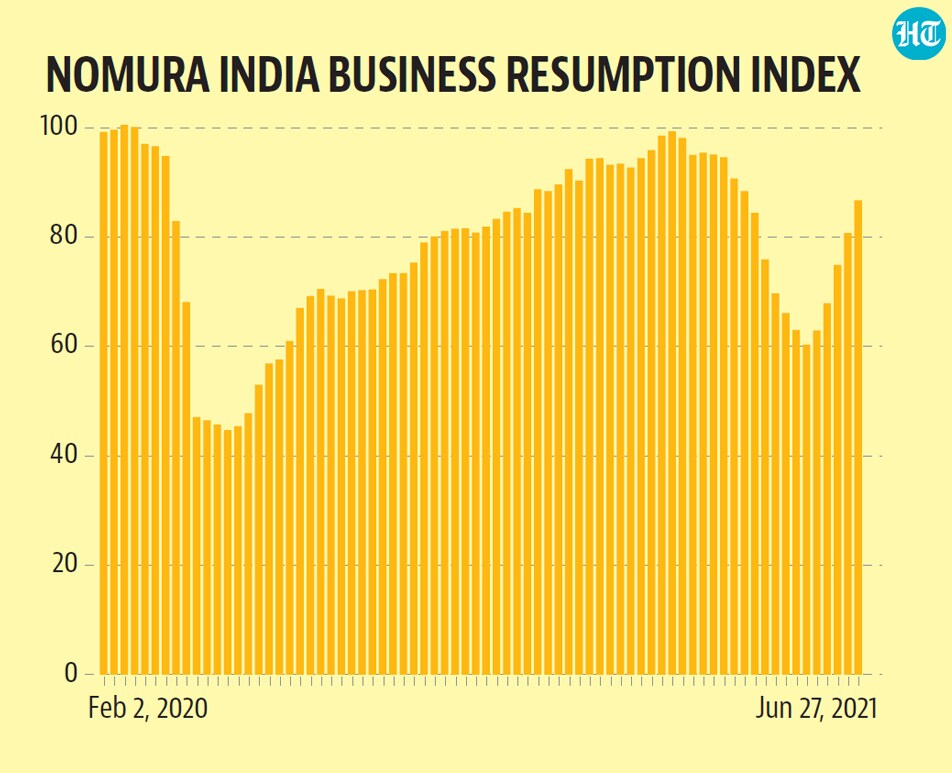

2. NIBRI's V-shaped recovery suggests the second wave did less damage

The V-shaped recovery in the Nomura India Business Resumption Index (NIBRI) is the closest to the narrative of the second wave’s economic impact being lower and short-lived than the first wave’s. NIBRI reached a peak of 99.3 in the week ending February 21 (100 indicates the pre-pandemic level). It started slipping gradually over the next month to reach 94.6 in the week ending March 28. Then, as the second wave gained momentum and mobility restrictions were re-imposed in most parts of India, NIBRI fell sharply to collapse to 60.3 in the week ending May 23. The second wave reached a peak on May 9, in terms of the seven-day average of daily new cases. The last few weeks have seen a sharp recovery, the highest in terms of week-on-week change, and NIBRI reached 86.7 in the week ending June 27.

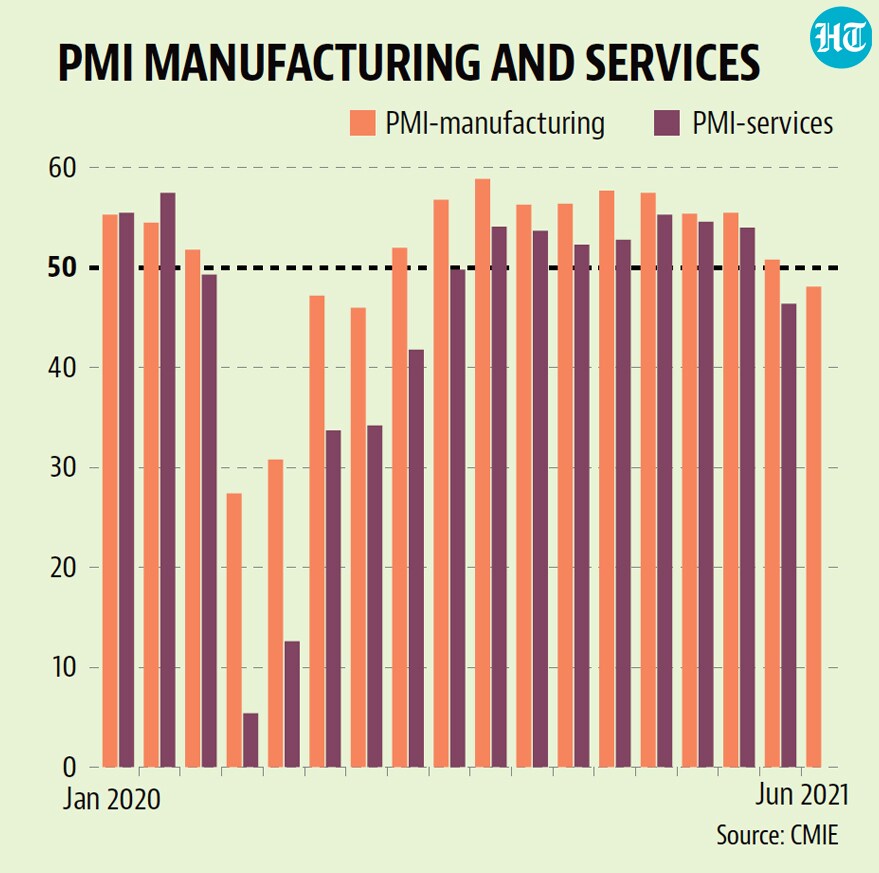

3. But the June PMI-manufacturing numbers raise a red flag on the demand front

Purchasing Managers’ Index (PMI) for manufacturing was 48.1 in the month of June. This is the lowest PMI manufacturing value since July 2020 and also the first time it has gone below the critical threshold of 50 during this period. A PMI value below 50 signifies a contraction in activity. The June numbers are cause for concern because PMI manufacturing did not fall below 50 even in the months of April and May, when the pandemic was raging. This suggests demand side rather than supply side (which is what lockdown restrictions create) headwinds to economic activity. “Growth of new orders, production, exports and input purchasing was interrupted in June as containment measures aimed at bringing the pandemic under control restrained demand. In all cases, however, rates of contraction were softer than during the first lockdown”, Pollyanna De Lima, Economics Associate Director at IHS Markit, the agency which conducts the survey, said in a release. Services PMI fell below 50 in the month of May itself. The June services PMI number will be released on July 5.

4. Capex numbers continue to disappoint

That there will be sequential recovery every time a lockdown is lifted is a truism. The question, as far as the economy is concerned, is the long-term effect of the pandemic on India’s growth prospects. Investment is among the biggest determinants of future growth. Whether or not businesses make investments depends on their assessment of the future prospects of the economy, which is what drives future demand.

The Centre for Monitoring Indian Economy (CMIE) capex database shows that the investment mood continues to be subdued. The year-on-year growth numbers are impressive for the private sector, largely because of a base effect. But new investment announcements, which are an important metric of business sentiment about future demand, continue to be at low levels compared to the pre-pandemic phase. What is also a matter of concern is a continuing weakness in new investment announcements by the government as well, which could be a result of strained state government finances. It is the states which have done most of the heavy-lifting during the pandemic. There is a further concern about the future, one summed up by Pranjul Bhandari, Chief India Economist at HSBC Securities and Capital Markets India Private Limited in a note in which she speaks of the recent pick-up in vaccination rate and the expectation that a “critical mass of the population is likely to be fully vaccinated by end-2021”.

“The second wave is receding but worries about a third wave abound. The direct cost of the second wave in 1QFY22 is likely to be half of the first wave. But the indirect cost of uncertainty is likely to be higher this time around, making pent-up demand in 2Q only half as strong as during the first wave”.

The note is hopeful that the “vaccination-led expansion” in the second half of the year will more than compensate for the “uncertainty-led sequential contraction,“ in the first half. HSBC estimates GDP to grow by 8% in 2021-22.

Which is high, but not as high as RBI’s current projection.